I published my list of 50 takeaways about working in venture capital in June 2022.

It’s still the most popular piece of content we’ve ever shared.

Here’s an updated version of that list with more things I’ve learned or noticed over the past year.

If you think I’m right, wrong, or anything in here resonates with you, let me know in the comments.

**This post has been updated with more learnings in this Twitter thread.

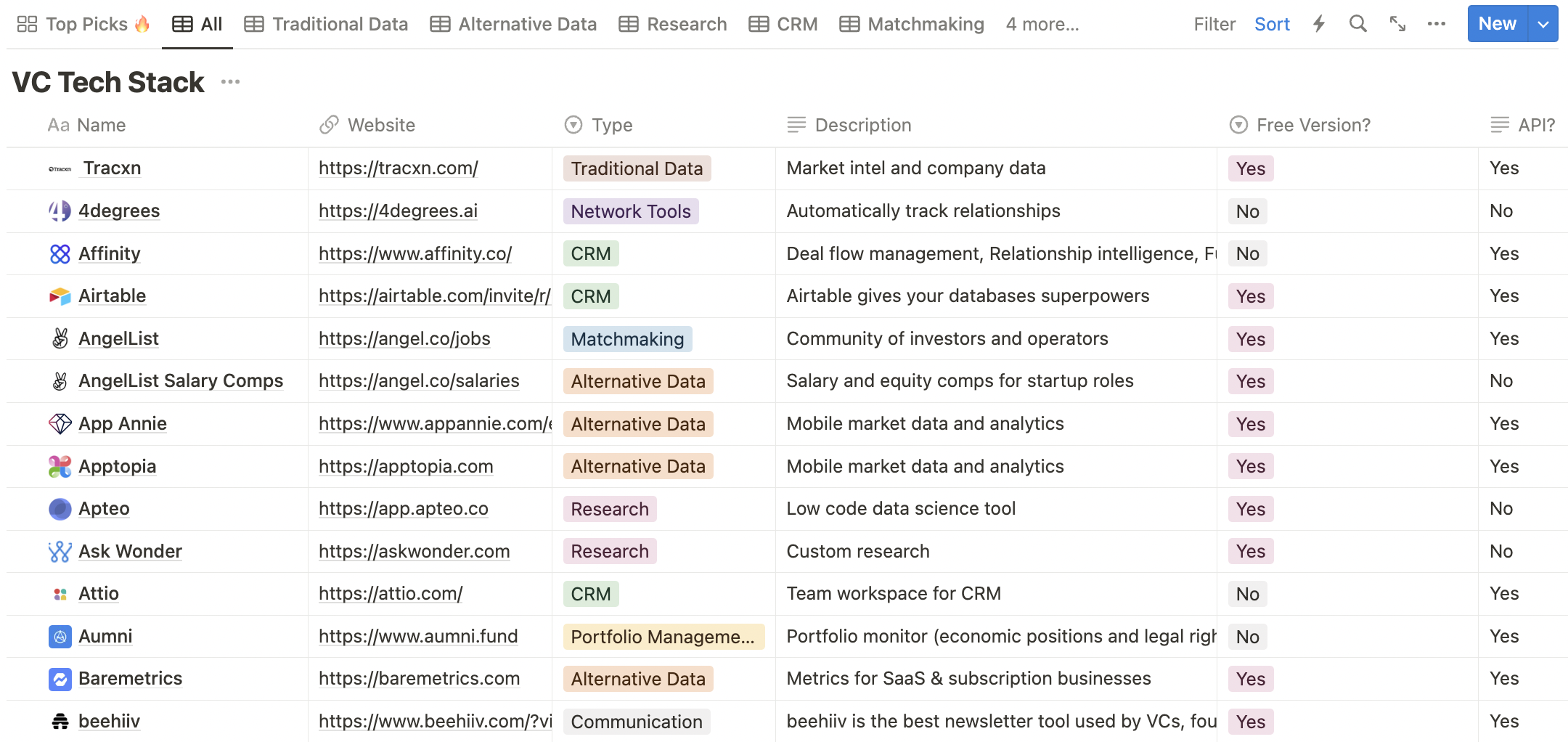

VC Tech Stack: 88 tools used by tier one VCs

Investment Memo Template: our boilerplate template for memos

Venture Media List: 132 people and places to learn the game

ChatGPT Prompts: prompts to give VCs more leverage

Diligence Question Bank: 84 questions to ask founders

Good news: We talk to and study some of the best VCs in the world every week. This gives us a behind-the-scenes look at how venture capital actually operates.

More good news: We share what we learn every week. If you want to impress your boss with your VC knowledge, look no further.

EVEN MORE good news: It’s free.