This week’s deep dive is on Arthur Patterson, co-founder and lead investor at Accel.

Arthur is one of the godfathers of Silicon Valley. He started Accel with Jim Schwartz back in 1983, and he has grown it quietly since then into one of the most-respected funds in the world.

Similar to some other investors we have studied, Arthur is not very loud online (noticing a trend?), and he has been selective with when to do public speaking appearances.

Here are some of our favorite lessons, quotes, and additional reading from studying Arthur.

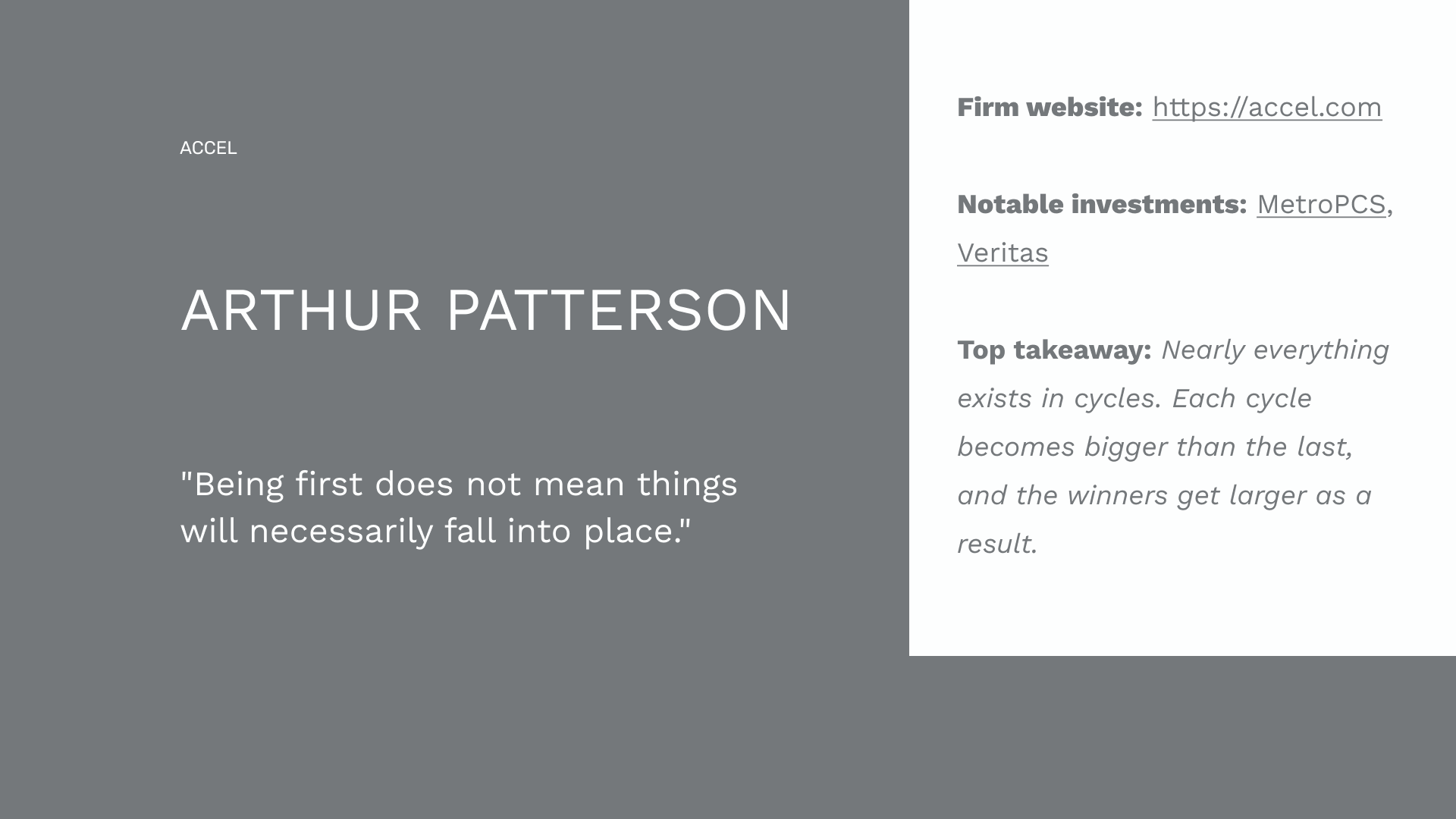

"Being first does not mean things will necessarily fall into place."

“The venture business has a pattern of roughly eight years of growth followed by six years of retrenchment.”

"Best venture investors are those that form partnership relationships with entrepreneurs and help them avoid a lot of mistakes. Doing this reinforces naturally good analytical judgement."

"At the early stages, unless you run a very tight experiment, you don't learn anything from it."

We started our careers in venture. After about a week, we had a realization.

We had no idea what we were doing.

Turns out, we weren’t alone.

Junior VCs don’t get training. You’re forced to figure it out on your own.

Learning the rules, tools, and players takes FOREVER to learn. That’s why we made the ultimate VC resource library to speed up the learning curve.