506b vs 506c: What Fund Managers Need to Know Before Efffectively Launching Their First Fund

If you’re fund manager looking to launch your first fund, you’ve likely heard of rule 506(b) and rule 506(c).

But just what do they mean, exactly?

Rules 506(b) and 506(c) allow GPs of such funds to bypass stringent regulations that public offerings typically involve, ultimately providing two easy avenues for raising capital more quickly. These rules are put in place by the Securities and Exchange Commission, and they are meant to protect non-accredited investors.

In this post, we’ll break down rules 506b vs 506c, and we’ll provide you with what you need to know to stay compliant during your fundraise.

Rule 506(b) is a rule under Regulation D of the Securities Act of 1933 that allows accredited investors to purchase securities from private companies, including equity and debt securities such as stocks, bonds, and notes.

With rule 506(b), companies are allowed to sell securities to accredited investors, but cannot solicit investors by advertising their securities offering publicly.

Additionally, the company is only allowed to accept investments from up to 35 non-accredited investors in any particular round of financing. These non-accredited investors must be sophisticated, meaning they must have ample knowledge and experience in financial and business matters of investing to make them capable of evaluating the investment’s economic risk.

This means that the accredited investor pool must be carefully managed and monitored to stay compliant with the regulations outlined in the rule.

Who can invest in 506(b) securities offerings?

Rule 506(b) securities offerings are available for accredited investors only (and a maximum of 35 non-accredited investors, who are considered sophisticated investors).

To be accredited, backers must have a net worth of at least \$1 million, excluding the value of their primary residence, or have earned an annual income of at least \$200,000 (or \$300,000 together with a spouse) in each of the past two years and have a reasonable expectation of achieving the same level of income in the current year.

Rule 506(b) has proven to be a highly beneficial exemption for companies looking to raise money without having to navigate the complexities of a full-fledged SEC registration.

Accredited investors can purchase securities from private companies, allowing them to invest in options not available in public markets.

Additionally, accredited backers can benefit from the potential of higher returns due to their knowledge and expertise in investing in private securities.

Rule 506(b) offerings are not regulated by state blue sky laws, which are state regulations established as safeguards for shareholders against securities fraud.

GPs are not responsible for verifying accreditation as investors can self-verify their accreditation status.

506(b) limitations

Rule 506(b) has certain limitations, which can be challenging for companies trying to raise funds.

One of the main drawbacks is that companies cannot publicly advertise any prospective investment – they are only allowed to solicit accredited investors. This means that fund managers have limited access to potential shareholders and must be selective in who they target.

They are also limited to a maximum of 35 non-accredited investors in any particular round. This can be restrictive for companies looking to raise large amounts of capital.

What is Rule 506(c)?

Rule 506(c) is also an exemption from registration under the Securities Act of 1933 which was introduced in 2013.

It allows issuers of private securities – including general partners (GPs) of private funds – to advertise their offering to accredited investors and generally accept investments from unlimited accredited investors.

Who can invest in 506(c) securities?

Accredited investors are eligible to invest in 506(c) offerings. However, unlike with the 506(b) exemption, the fund’s GP must take “reasonable steps to verify” that purchasers are accredited investors.

506(c) benefits

Accredited investors can purchase securities from private companies.

GPs have unlimited access to potential accredited investors because the companies are permitted to publicly advertise their securities offerings.

Additionally, hedge funds, private equity companies, and other accredited investors can access a larger pool of capital when using Rule 506(c). This can be beneficial for private fund managers who are looking to raise more capital in their financing rounds.

506(c) limitations

The main limitation of Rule 506(c) is that accredited investors must be verified to invest. Issuers must take reasonable steps to verify accredited investor status, which involves obtaining supporting documentation and conducting due diligence. This can be a time-consuming process and can significantly slow down the capital-raising process.

Another drawback of Rule 506(c) is that companies are not allowed to solicit non-accredited investors. This means that companies that use this exemption will have a smaller pool of potential shareholders to target.

How can the GP verify LP accreditation for 506(c) investors?

The GP of a private fund must take reasonable steps to verify the accredited investor status for 506(c) investors.

This can involve obtaining supporting documentation and conducting due diligence. The GP can have accredited investors submit documents such as tax returns, independent CPA letters, and/or bank statements to verify accredited investor status.

The GP should also take steps to ensure that accredited investors are not purchasing securities on behalf of non-accredited investors.

Additionally, the accredited investor must provide written representations and agreements verifying their accredited investor status.

Form D

Companies that heed the regulations of Rule 506(b) and (c) may sidestep SEC registration for their securities offering but are required to submit a “Form D” notification electronically afterward.

This document contains pertinent and basic information such as promoters’ identities, executive officers’ & directors’ addresses plus some essential details about the sale – although it doesn’t provide in-depth insight into the company itself.

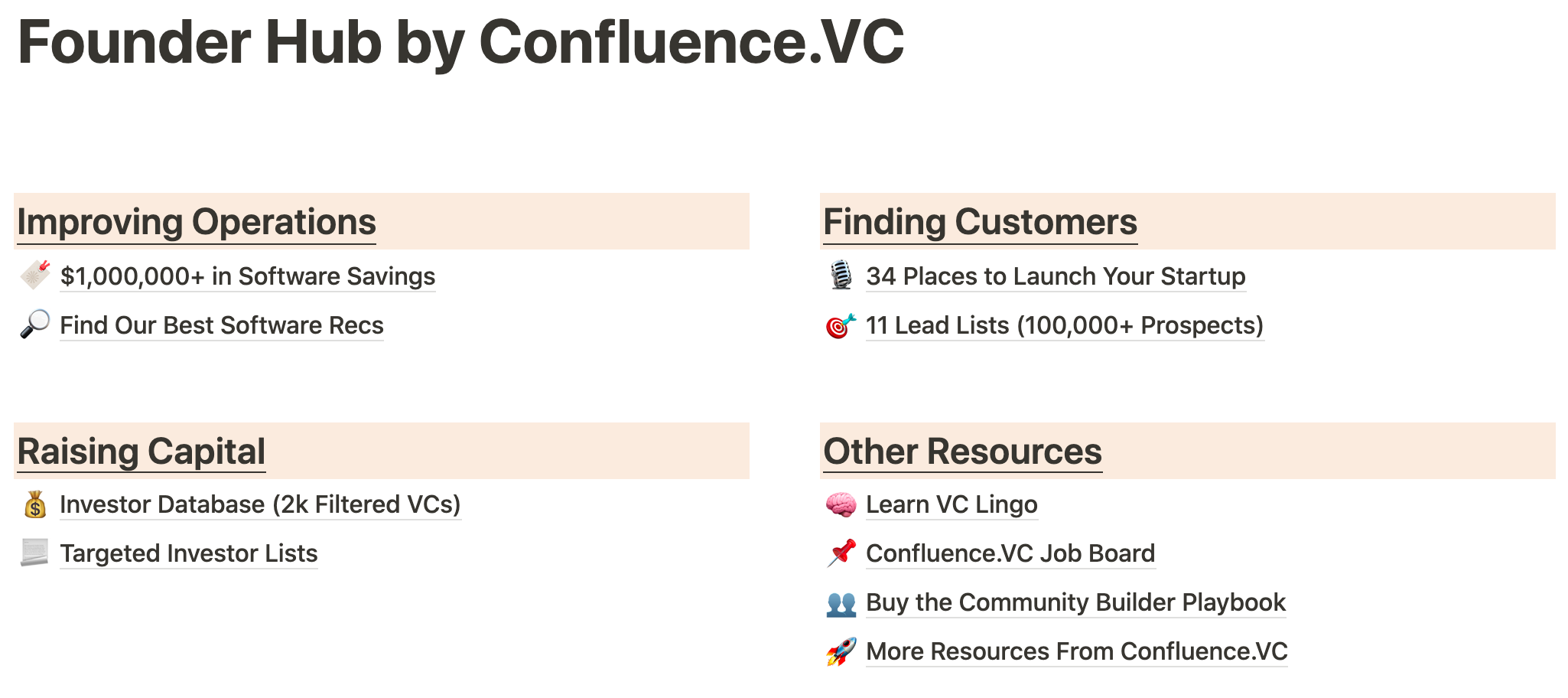

Feeling stuck as a founder? Get Founder Hub by Confluence.VC to change that.

506b vs 506c: bottom line

If you’re a fund manager who is looking to raise capital for your company, you may want to consider using regulation 506(b) or 506(c).

These regulations can help you raise the money that needed to get your business off the ground. Keep in mind that some requirements must be met for these regulations to apply. Be sure to consult with a legal professional before moving forward with this process.

An operating agreement is a legal document used by companies to define their organizational structure, roles and duties of owners and other key parties involved in the business, and methods for handling all transactions that occur within the company.

Stock options in startups work as a form of equity payment that allows an employee to purchase a certain number of shares of company stock at a specified price.

An over-allotment option allows companies to issue extra shares of their stocks beyond those that they initially planned or announced when they go public (or offer other securities). It’s also known as a “greenshoe option”.

Participating preferred stock is a type of preferred stock that gives the holder the option to receive dividends equal to or greater than the customarily defined rate at which preferred dividends will be paid to preferred shareholders.